The Molecule Is Fixed. Asset Value Is Not.

Why deeper early exploration creates asset value in biotech

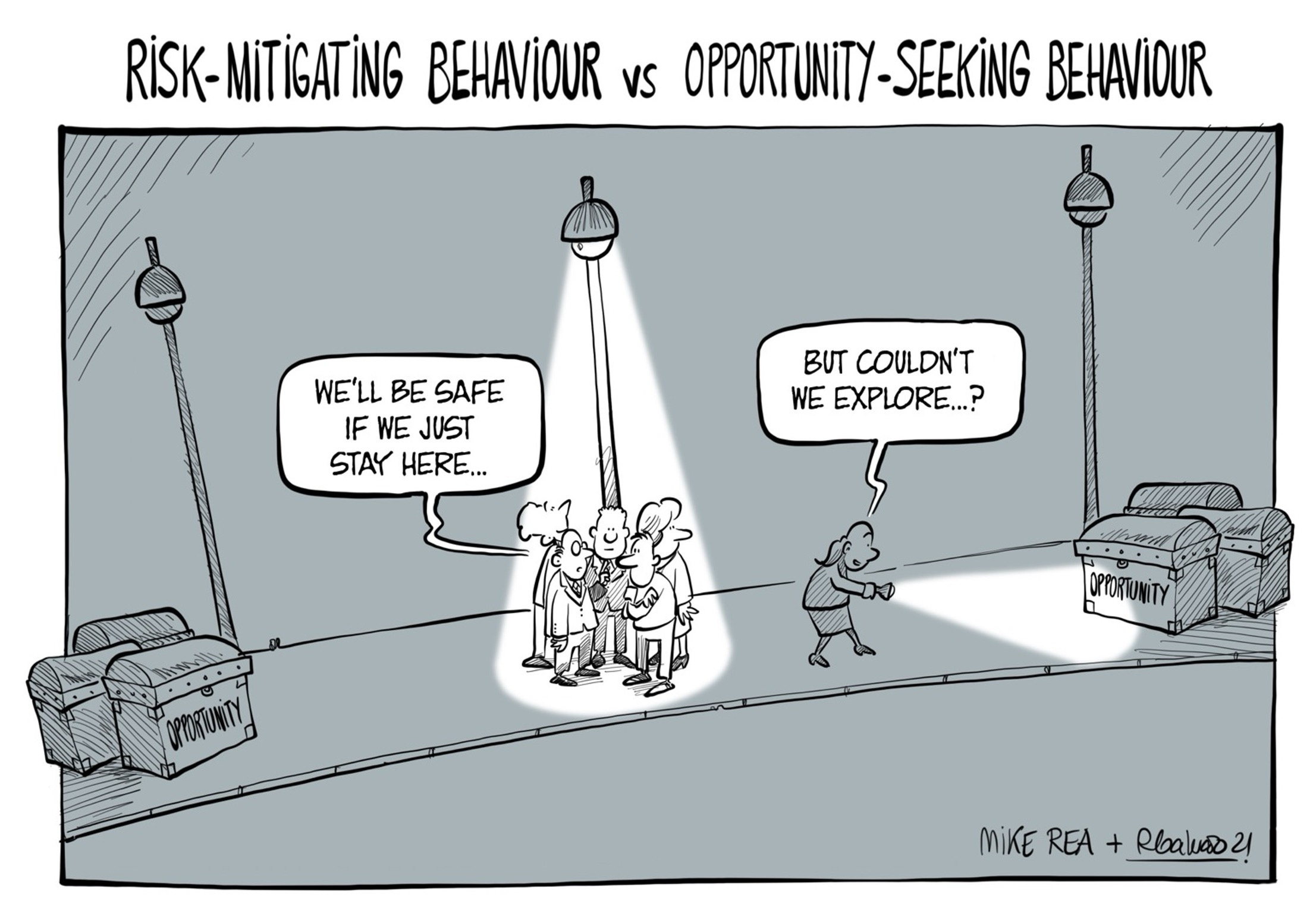

A reader pushed back on my earlier post, The Optionality Orchard, with a serious objection: biotechs cannot really afford to think in options. The drug will do what it will do.

At one level, that is true. A molecule is not a software roadmap. Management cannot will a biological outcome into existence. The mechanism will translate, or it will not. The safety profile will emerge, or it will not. The data will say what the data says.

But that objection misses where optionality actually sits in biotech.

Optionality is not about controlling the biology. It is about controlling the learning agenda around the biology. And in practice that matters because earlier, deeper learning can materially increase the pre-launch value of an asset.

It does so in two ways. First, it increases confidence in more than one strategically relevant direction. Secondly, it forces harder questions earlier, when the cost of answering them - and acting on the answers - is still relatively low.

That is not a philosophical distinction. It has direct implications for programme design, financing strategy, business development, and how an asset is priced by the market.

Biology is fixed. Strategic range is not.

The phrase “the drug will do what it will do” collapses two different issues into one.

The first is scientific uncertainty: what does the molecule actually do, in which patients, under which conditions, and with what magnitude of effect?

The second is strategic range: given what the biology reveals, how many credible paths does the company have to create value?

That range may include:

a faster first indication;

a narrower but more actionable biomarker-defined population;

a better sequencing strategy;

a combination path;

a partnering route with clearer proof points;

or, just as importantly, an earlier decision to stop.

The molecule may be fixed. But the set of credible actions available to the company is not fixed at the outset. It is shaped by what the company chooses to learn, when it chooses to learn it, and how well that learning is translated into a development and partnering strategy.

That is the real source of optionality.

The real risk is not lack of focus - it is false precision

Small biotechs are often told to stay focused. That advice is not wrong, but it is frequently misapplied.

In practice, “focus” can mean one of two very different things.

The good version is disciplined early design: asking the most decision-relevant questions as efficiently as possible.

The bad version is premature narrowing: building the company around one simplified proof-of-concept story before the underlying asset has been characterised deeply enough to justify that level of certainty.

That second version often looks tidy in a pitch deck. It can also be value-destructive.

A narrow early plan may produce a clean data readout for the next round. But it can leave critical questions unanswered:

Is the lead indication actually the best entry point?

Is the effect concentrated in a subgroup the current design will blur?

Is there a biomarker strategy that would materially improve the asset’s positioning?

Are there adjacent indications with faster regulatory or commercial paths?

Are there mechanism or safety signals that will matter later, but are cheaper to investigate now?

When those questions are postponed, they do not disappear. They simply become more expensive - scientifically, financially, and strategically.

How deeper early exploration creates asset value

The case for richer early exploration is not that more data is always better. It is that well-chosen early information increases the number and quality of credible future moves.

There are two main ways it does this.

1. It creates confidence in more than one value-creating path

An early programme that includes the right biomarker work, translational measures, secondary endpoints, or adaptive cohorts can do more than validate a single headline thesis.

It can also clarify:

where the biology is strongest;

which patients are most likely to respond;

whether there is a narrower, faster, or more defensible first indication;

whether the mechanism has relevance beyond the initial target setting;

and whether the asset supports a broader platform or follow-on story.

This is not “spray and pray” exploration. It is targeted effort designed to preserve credible choices until the evidence justifies narrowing them.

That matters because asset value is rarely driven by a single binary question alone. It is also driven by what a credible counterparty - investor, partner, or acquirer - believes could happen next.

A molecule with one plausible path may be interesting. A molecule with one plausible path plus two credible expansions, a clearer responder logic, and a better-defined development sequence is usually more valuable before approval, even if the underlying biological signal is unchanged.

2. It surfaces hard questions while they are still cheap

The second benefit is often underappreciated.

Deeper early work does not just reveal upside. It also reveals constraints.

It forces management, boards, and investors to confront questions that otherwise get deferred:

Does the mechanism really translate in the clinically relevant population?

Is the therapeutic window wide enough for the intended setting?

Does the biology point towards monotherapy, combinations, or a defined subgroup?

Are there resistance or durability issues that change the commercial case?

Is the large headline indication actually less attractive than a smaller, faster, better-defined one?

These are not side questions. They are the questions that determine whether a programme compounds value or burns capital.

When surfaced early, they improve asset allocation. Weak assets can be stopped sooner. Better indications can be prioritised earlier. Trial designs can be improved before large commitments are made. And partnering discussions can be framed around evidence rather than aspiration.

In other words, early depth does not just create upside optionality. It also reduces the cost of being wrong.

Why founders, BD teams, and investors should care

This matters differently depending on where you sit, but the underlying economic logic is the same.

For founders and management teams

Deeper early exploration improves strategic choice.

It can help a company avoid overcommitting to the wrong lead indication, identify a faster path to clinically meaningful proof, and build a more resilient narrative for future financing. It also reduces the odds that the company reaches a major inflection point with a dataset that is clean but strategically thin.

The practical benefit is not complexity for its own sake. It is better decision-making under capital constraints.

For BD teams

A richer early package makes an asset easier to position and easier to transact.

Partners do not just assess whether a programme has positive data. They assess whether they understand the mechanism, the responder logic, the expansion potential, the development risks, and the work still required after signing.

The more of that is clarified early, the more credible the asset becomes in a competitive process. That can improve terms, widen the pool of interested counterparties, and shift negotiations from “help us figure out what this is” to “here is where this can go next”.

For investors

The value of an early asset is not just the probability that the first proof-of-concept readout works. It is the probability-weighted value of the future strategic tree that the asset supports.

That includes upside breadth, downside containment, financing efficiency, partnering leverage, and the quality of future decision points.

An asset that has been explored narrowly may still produce a positive signal. But if it leaves too many high-value questions unanswered, the investor is still underwriting substantial hidden uncertainty. By contrast, a company that has used early capital to improve the shape of the uncertainty may deserve a better valuation even before the ultimate clinical answer is known.

If I was trying to persuade your board, here’s what I would say…

—

In biotech, we do not create value by pretending we can control biology - we create it by improving the quality of what we learn early, while learning is still cheap. A more deeply characterised asset gives us more than one credible path to value: a better first indication, a clearer biomarker strategy, stronger partnering leverage, and earlier kill points if the thesis is weak. That does not require undisciplined expansion. It requires disciplined early design aimed at reducing the uncertainties that matter most to valuation, development strategy, and deal terms. The molecule may be fixed, but the value we can build around it is not.

This is not a call for undisciplined expansion

None of this means early programmes should become sprawling.

It does not mean adding endpoints indiscriminately, chasing every weak signal, or pretending every molecule is a platform. And it certainly does not mean small biotechs should spend as if capital were abundant.

The point is more practical than that.

The goal is to identify the highest-leverage early questions - the ones that can most improve asset value, development quality, or negotiating power per pound spent - and design the programme so those questions are answered as early as reasonably possible.

Sometimes that means biomarker work. Sometimes it means richer translational sampling, smarter cohorts, better endpoint architecture, or cleaner archival of data for later repositioning. The specific tools matter less than the discipline behind them.

The best early programmes buy information asymmetrically

That, ultimately, is the point.

The best early biotech programmes do not just buy progress. They buy information asymmetrically.

They spend relatively modest amounts of capital to answer questions that would become far more expensive later. They improve the company’s ability to choose between indications, refine development strategy, structure partnerships, and abandon weak paths before they consume disproportionate resources.

So when someone says a biotech cannot afford to think in options, I think the more relevant question is: can it afford not to create them where they are cheapest?

Not because optionality changes the biology. It does not.

But because it changes how much strategic value a company can extract from what the biology eventually reveals.

I think both the statements can be true. At one level, the generation of clinical data is invariably a catalyst for additional fund raising as a biotech hits an inflection point. This should provide optionality either to explore additional indications with a lead asset or to accelerate the development of a follow-on drug. Argenx is the poster child for such an approach.

However, you do have to be lucky in the timing. Biotech could be out of favour, generalist investors could be reluctant to pour in etc.

At a deeper level a company that is laser focused on getting from A-B (no doubt backed by their existing investor base) may miss the wood for the trees and leave possibilities to be explored by others.

Perhaps it comes down to communicating a clear message from the outset and deciding which kind of Biotech you aspire to become.